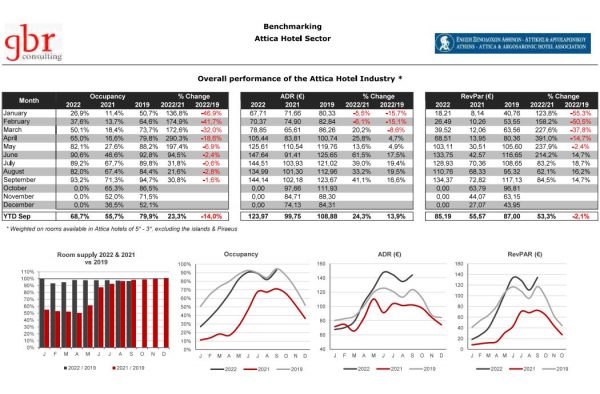

The data collected monthly by the Athens Attica and Argosaronic Hotel Association (EXAAA) in collaboration with GBR Consulting show for Athens hotels average occupancy close to 2019 levels, especially in the months of July 2022 (deviation from 2019 of the order of 0.6%) and September 2022 (deviation from 2019 of the order of -1.6%).

However, as pointed out in the relevant press release, the signs of average occupancy are still negative, both per month and overall (-14%) compared to 2019.

Average room rate and revenue per available room

Regarding the average room rate (ADR) and the revenue per available room (RevPar) of the hotels, the improvement trend is evident here as well, especially in the quarter of June-July-August 2022, which is however considered reasonable and expected due to of the summer season and the increase in tourist flows to our country.

In September 2022, however, there is a slight decline in performance in ADR and RevPar. The overall positive course of the specific indicators from April 2022 onwards clearly contributed to a total average price increase (ADR) of 13.9% for the 9 months, while the revenue per available room remains negative (RevPar / -2.1%).

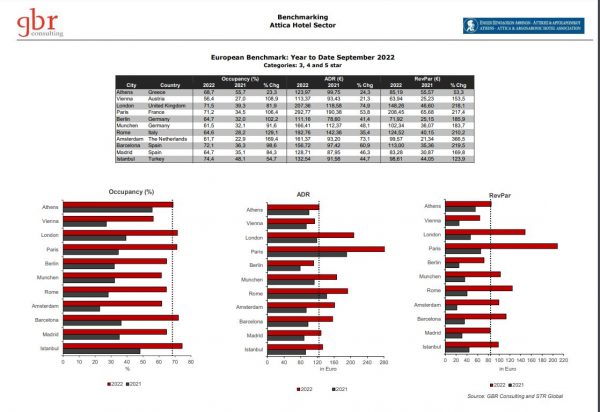

Athens’ competitors

As far as Athens and its competitors are concerned, we notice that Athens in the month of September, with an average occupancy of 68.7% (an increase of 23.3% compared to 2021), is in the last position – positive – change compared to other competitor cities. With an average room rate / ADR of €123.97 (an increase of 24.3% compared to 2021) it is in the penultimate position in -positive- ADR change against its competitors – as the lowest average room rate is €113.37 (Vienna) and the highest reaches 292.77 euros (Paris).

With a revenue per available room / RevPar of 85.19 euros (an increase of 53.3% compared to 2021) it is in the last position of -positive- RevPar change compared to the rest. In conclusion, the peculiar for tourism year of 2022 was perhaps a little more special, for Athens – and less so for its competitors.

Room for improvement

The above data highlight the many opportunities for further improvement of the position Athens in the European and international tourism market and the particular importance of the significant investments and projects of special and general infrastructure that are launched either by private initiative or by regional, municipal, local and other institutions.

It is necessary to speed up the implementation of infrastructure, whether planned, or not, to strengthen and enrich the proposal of Athens in the wider region and above all, they underline the need for unity and mobilization among all those working to benefit the Greek capital.

At the same time and in view of a series of assumptions for the rest of 2022 and for the whole of 2023 – such as the oversupply of tourist beds, high energy costs, therefore by extension the high costs of supplies and operation of the hotel businesses, in combination with the uncertainty about the war and the pandemic – it is necessary for State and Tourism bodies to jointly investigate , as soon as possible, best ways and practices to protect all categories of Athens hotel businesses.

![Διακοπές: Πού ξόδεψαν 3,68 δισ. οι Έλληνες – Η μέση ημερήσια δαπάνη [γραφήματα]](https://www.ot.gr/wp-content/uploads/2026/03/tourismos_ar.jpg)