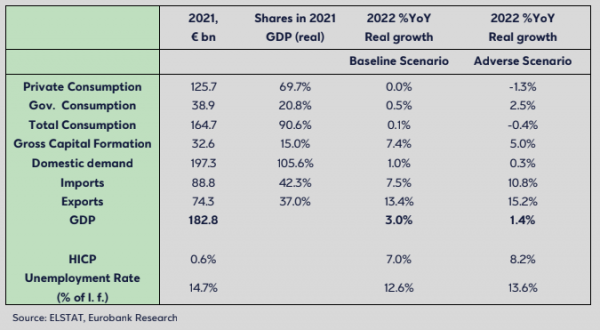

Eurobank “sees” growth of only 1.4% for 2022, according to the adverse scenario in its study entitled “Interim Report on the Development of the Greek economy in 2022″, with average inflation reaching 8.2%.

At the same time, the bank’s basic scenario predicts GDP growth of 3%, but also high inflation of 7%.

Conditions

According to the study, the unfavorable scenario assumes prolongation of the war and economic sanctions, leading to a larger supply shock, manifested by higher energy prices. In turn, this means higher and more persistent inflation (and consequent income erosion), more prolonged investment deferrals, lower external demand and more fiscal support measures. Overall, this leads to an increase in real GDP of 1.4% on an annual basis in 2022. The magnitude of the difference between the baseline and the adverse scenario is due to the nature of the supply-side disruption that is assumed and, therefore, does not try to approach the worst case scenario, ie a cumulative effect of many negative factors.

Baseline scenario

Beyond that, the baseline scenario approaches the supply shock caused by rising energy prices on the assumption that war will not escalate and that the EU sanctions against Russia, the fiscal support measures of the Greek government and the normalization of monetary policy will remain at the levels known until May 2022.. Overall, this scenario leads to an increase in real GDP of 3.0% on an annual basis in 2022 and a rate of change in the HICP by 7% (with upside risks). Although this growth rate falls short of pre-war forecasts, unemployment is improving due to the effects of the base (lower unemployment in 2021) and ongoing support measures.

Dynamic start

According to the bank, the Greek economy, after a rapid recovery in 2021, had entered 2022 with the precursors indicating prospects for dynamic growth. However, the war in Ukraine, also in the whole European economy, negatively affects the short-term and medium-term outlook, causing a slowdown in growth in the short term and an increase in inflation compared to previous forecasts. long term. The magnitude of the impact will depend on many factors, such as the duration of the war, the final mix and duration of EU sanctions, and monetary and fiscal policy measures.

Impact due to war

The immediate impact of the crisis is limited as trade, tourism and economic relations with Russia and Ukraine are relatively small: exports of goods and services to Russia and Ukraine as a whole accounted for about 2.1% of the total in 2019, ( the same share for tourism revenues) and no Greek bank has a significant presence in these countries.

However, there are notable channels of indirect impact, such as (a) disruption caused by war in supply chains, external demand and world trade routes; (b) supply-side disruption by rising energy prices: Greece is exposed to Russian imports in its energy mix as 73% of imported oil and 39% of natural gas in 2020 came from Russia.

Although there are alternative sources for substituting Russian imports so that energy security is not jeopardized, increases in energy prices are fueled by secondary increases in prices for goods and services. This exacerbates the inflationary pressures that had already manifested themselves before the war as a result of extremely accommodative monetary and fiscal policies in the aftermath of the pandemic.

Inflation, in turn, erodes disposable income and puts pressure on the current account balance, especially as a significant part of imports concerns energy products, c) increased uncertainty can cause short-term deferral of consumer and investment decisions and in the cost of borrowing for State and private sector.

Counterweights

On the other hand, the Greek economy has significant counterweights that support the short-term outlook: (a) there are expectations for a strong tourist season, provided that a worsening of the situation in Ukraine is avoided. Also, the latest information shows undiminished activity in several other sectors, (b) Greece will benefit from a Recovery and Sustainability Fund (largest beneficiary in the EU as a percentage of its GDP), the NSRF 2021-2027 and EIB funds, a total of approximately € 90 billion available over the next 5 years.

These funds, together with the mobilized private and banking funds, have the potential, not only to provide great liquidity, but to activate the transformation of the productive model of Greece towards sustainable development based on exports and investments.

However, to achieve this, it is important that resources are effectively channeled into selected economic activities, in particular green transition and digitization, and that they are accompanied by a forward-looking and ambitious implementation of the structural reforms that accompany the disbursement of funds. (c) the economy enjoys a very comfortable liquidity position: around € 34 billion of new deposits have accumulated in the pandemic with the help of fiscal support measures, the state has a liquidity cushion of around € 38 billion, around € 38.5 billion DSBs will be flexibly reinvested in the ECB Pandemic Liquidity Program by the end of 2024 supporting financing costs and banks will draw liquidity from targeted liquidity delivery operations (TLTROs), (d) fiscal measures to reduce energy costs for energy and businesses worth around € 7.5 billion by May 2022. These come in addition to Covid-19-related € 43.3 billion support measures between 2020 and 2022, of which € 4.1 billion billion for 2022.

Nevertheless, it is important to stress the need to control the budget deficit in 2022 and return to a primary budget surplus in 2023 in order to maintain market confidence, especially due to deteriorating financial conditions, and to facilitate the recovery of the Greek economy. Fiscal stability is also a prerequisite for controlling the current account deficit, which is growing.